“Money, money, money. It’s so funny, it’s a rich man’s world,”sang Abba.

Indeed, it even made someone president. However, at this stage of my career (i.e. poor and limited resources), what’s more relevant to me is to be able to maintain my finances well so that I can one day become rich. Having found that this is a common problem among entry level professionals, I thought that it might be useful to share with you how I manage my money.

Before we proceed though, there are definitely competing views about saving. Choosing whether to save and how much to save is very personal to each individual. Some people want to save for a better life in the future whilst some people don’t save at all because they want to live better in the present. I know some of my colleagues who don’t save because they believe that there’s no point saving now. It’s better and easier to save once you rise to a certain grade. My personal view is that while I recognise the importance of living in the present, I believe that when I do the little things well when I have little, I will be able to do more when I have more. It’s a similar work ethic I have when it comes to me being given small mundane tasks as a junior (see here for more). Hence, without further ado, let me open my bag of tips and tricks…

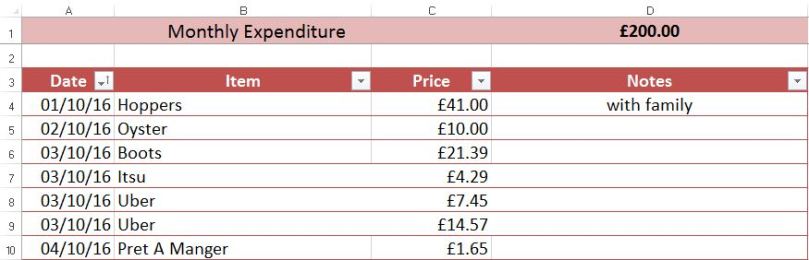

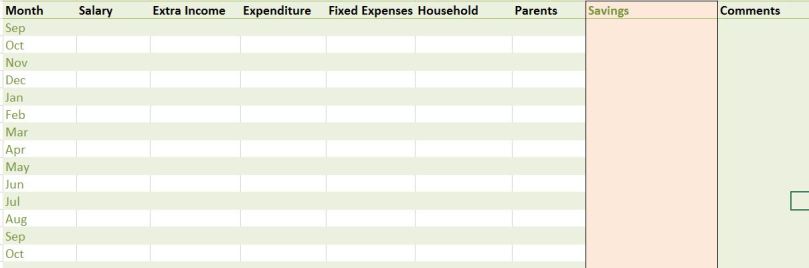

1a. Using Excel to track your expenditure

Generally, a good target to start with is to save 5% then 10% and eventually 20% of your net monthly salary. I save around 15%-20% each month and I think that’s an appropriate amount given that post tax, I have almost nothing left with rent and expenses 😦

Excel is actually easy to use if you know how to do the basic “=SUM()” and that’s pretty much all you need. All you need to know is how much you’re spending and how much you’re saving. You don’t need to manually key in all the items you’ve spent your money on if you use card, because most UK banks can give your bank statement in .csv format, which is essentially Excel and thus, you can just copy and paste into your own spreadsheet.

However, because I have quite a few bank accounts, I have to reconcile them. I also do a “Snapshot” spent to see what I have in the bank vs what I have supposedly saved. This is very useful especially in cases where you are setting aside money for something. For example, I send money back home every few months because it just makes sense to do so for exchange rate purposes, instead of once every month.

I have been tracking my expenses for the past 4 years but the level of commitment to do this every week has increased because now it’s my money that I have to manage.

Sorry mum!

1b. Making use of existing market tools to help you

Apps such as Wally can help you track and plan your budget. It has a colourful and user-friendly interface and breaks down your expenditure into different categories so you can identify what you are spending most on. However, I think the common problem is that you have to manually key in all your costs immediately or possibly forgetting to add some items at the end of the day.

If you use credit card to pay for most of your purchases, some cards like American Express will automatically track your expenditure and even produce a pie chart which analyses your spend. If you’re even more advanced and you want on the spot analysis, there’s Monzo bank. Once you use it to pay, it’ll automatically appear on the app. It also has a feature that predicts your next spend. Amazing what technology can do.

2. Regular Monthly Saver

How do you start saving? In my opinion, the easiest method is to open a Regular Monthly Saver because it forces you to put aside money every month. Fortunately, UK banks have really good current account interest rates. I have three bank accounts, Halifax (£5 monthly reward), Lloyds (£7 monthly) and TSB (£14 monthly). It’s a little bit of a hassle though because you need to make sure each account has sufficient funds to do the direct debits and transfers. If you’re generally not a person who is very diligent with checking your bank accounts, I would suggest that you should have a maximum of 2 bank accounts. Three is bit too much.

For Singaporean readers, don’t let low interest rates deter you though, hunt around for good bank accounts where you can put your money in. I heard that OCBC 360 account and Bank of China have pretty good deals.

3. Other useful apps

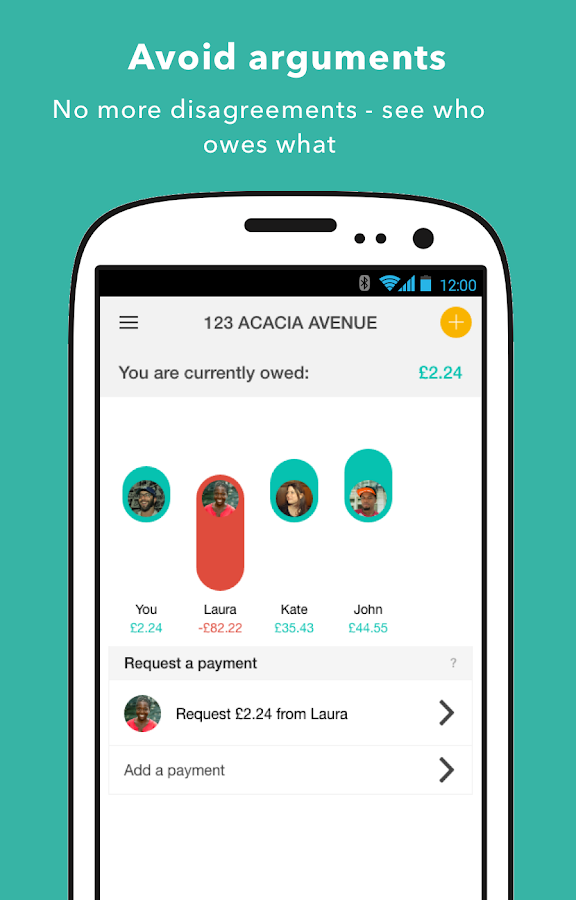

For every awkward conversation you avoid with those same few friends who owe you money, fear no more!

Introducing…

Spilttable!

It’s an app that keeps track and calculates how much you owe each other. I currently use this with my housemates. The only catch I have with this app is that it doesn’t separate month by month, which makes it challenging for me to do my expenses – it merely squares out how much you owe each other when someone has paid for the rest. Splittable can even do payments in-app to your housemates now, and also has a built in Bizzby (app that allows you to hire cleaners, plumbers etc) tab!

4. Other investment products

Invest in Blue chip company stocks if you’re risk averse. Personally, I don’t have enough money to think about those. But honestly, when Brexit happened, I know of a few people who hedged the pound using USD and didn’t suffer as much a loss as I did. Opening a trading account is not difficult – you just need to take the first step to do so.

“All the things I can do if I have a little money. It’s a rich man’s world.”

I don’t agree that one must be rich in order to start doing things but unfortunately, there are more things that you can do if money is not constantly at the back of your mind. Living in London has completely convinced me of that – there’s only so much I can do without spending too much money. But I guess the point is to first start looking to do things in order to gain a little money. There’s a lot of inertia to start doing something about your financials. However, if you don’t start doing things to improve your financials, I’m pretty sure you won’t be able to handle it when you get a lot of money… because it’ll just disappear anyway.

Unless you get to the point to pay people to manage the money for you. Then I guess why not!

–

Hope you enjoyed the post! I would also like to hear your thoughts so please leave a comment. You’ll never know who else is reading your comments and might benefit from them!

If you would like to stay tune to the next post, please click the “Follow” button on the bottom right of the page and just provide your email. You don’t need to have a registered wordpress account.

You can also connect by following my instagram @twentyandfabulous and liking my facebook page https://www.facebook.com/twentyandfabulous/

Stay fabulous & financially savvy everyone!

Athena